Learn how the most important greenhouse gas reporting schemes work, and see how Ducky's climate calculator fits in

Greenhouse gas reporting schemes vary widely in their methodologies, meaning they are often incomparable. They are also often open to subjective interpretation (or misinterpretation), leaving some of the most impactful decisions completely up to the reporter. As such, they can’t be readily used to assess whether an entity is sustainable or not. In particular, it’s near impossible to assess whether a sold product or service is sustainable. However, we aim to make the best out of what we have!

Ducky has chosen to follow the GHG Protocol when we supply data for greenhouse gas reporting. We continuously update our offerings to adhere to the reporting requirements that are being introduced through the European green deal over the next few years. See also the Norwegian government's info page about the EU taxonomy for the legal status right now.

What is the GHG Protocol?

The World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD) created the GHG Protocol to help countries and companies account for, report, and mitigate emissions. Launched in 1998, the GHG Protocol defines a standardised framework for managing and measuring emissions from private and public sector operations, value chains, products, cities and policies to enable greenhouse gas reductions across the board. It classifies GHG emissions into three “scopes” (scope 1, scope 2, and scope 3) to improve transparency and provide utility for different organisations and business goals. The standard’s primary audience is businesses developing a GHG inventory. However, all kinds of organisations that give rise to GHG emissions can use this standard, e.g. NGOs, government agencies and universities.

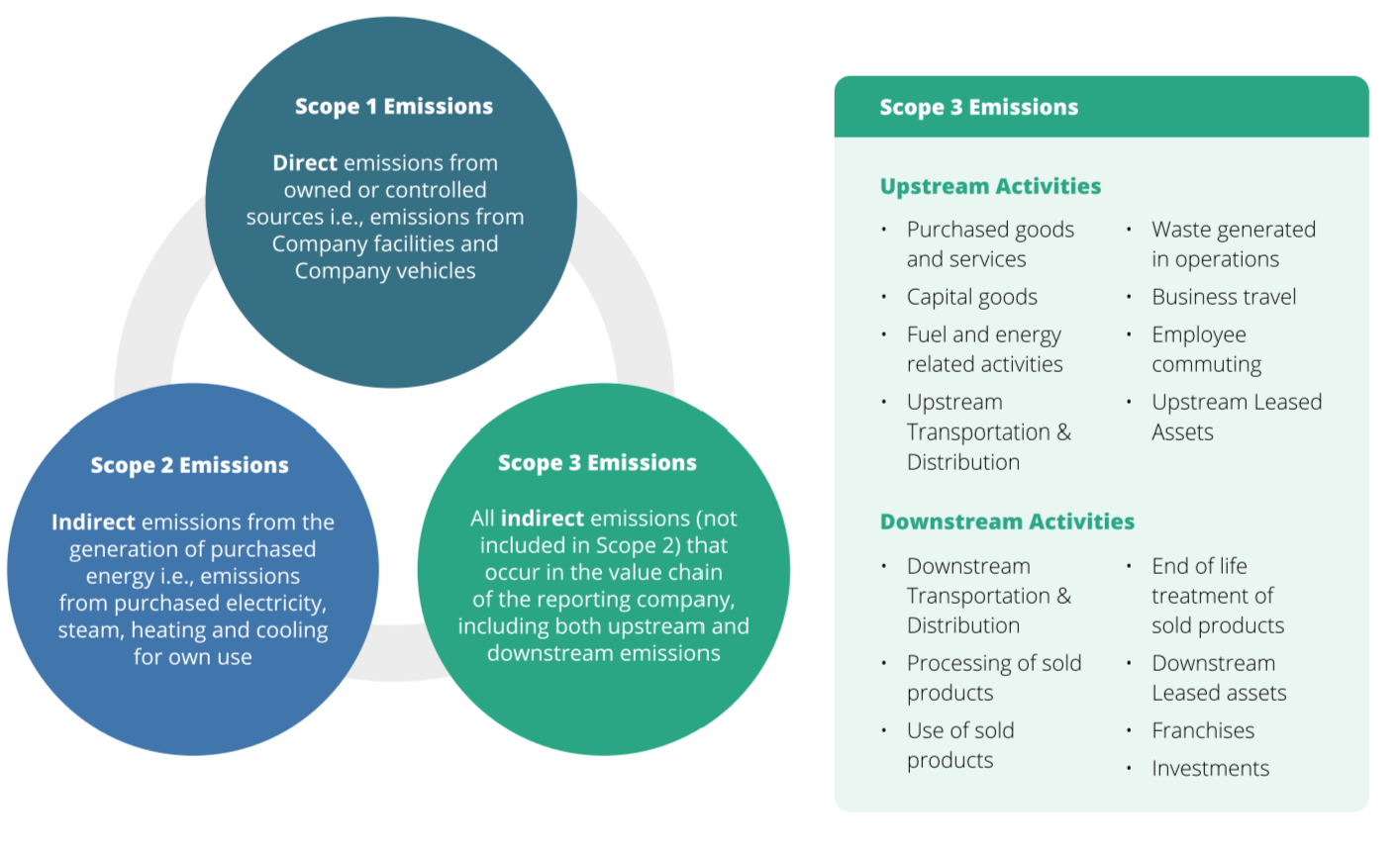

Figure: Definitions of Scope 1, 2 and 3 emissions (left); Scope 3 emissions categories (right). Source: Wrap Scope 3 GHG Measurement & Reporting Protocols.

Scope 1, 2 and 3 emissions

According to the GHG Protocol Corporate Standard, a company’s greenhouse gas emissions are classified into three scopes: Scope 1 emissions are direct emissions from owned assets. In other words, emissions are released into the atmosphere as a direct result of a set of activities, at a firm level. Scope 2 emissions are indirect emissions from the generation of purchased energy (electricity and heat). Scope 3 emissions are all indirect emissions (not included in scope 2) that occur in the value chain of the reporting company, including upstream and downstream emissions. Scope 1 and 2 emissions are mandatory and rather easy to calculate, whereas Scope 3 is voluntary and very hard to monitor.

Head over to our specific articles for details on the reporting standards:

- An intro to Scope 1 GHG emissions

- An intro to Scope 2 GHG emissions

- An intro to Scope 3 GHG emissions

- Scope 3 GHG reporting in the food and drink sector

Head over to our guide on company level emissions reporting and see our endpoints to deliver reporting to read more about this use case and get started.

Overview of standards

Global standards

|

Name |

Target audience |

About the standard |

|

General |

|

|

|

General |

|

|

|

Organisations, public sectors, municipalities, companies |

|

|

|

Companies |

|

|

|

Companies |

|

|

|

Accounting |

|

|

|

Public and private sector |

|

|

|

Municipalities, cities, states, organisations, companies |

|

Norwegian and nordic standards

|

Name |

Target audience |

About the standard |

|

Municipalities, counties, companies |

|

|

|

Klimakost, Asplan Viak |

Municipalities, companies |

|

|

TCFD guide, Finans Norge |

Finance, companies |

|

|

Nordic Sustainability Reporting Standard (NSRS), Regnskap Norge |

Small and medium-sized companies |

|

|

The Norwegian Environment Agency (Miljødirektoratet) |

Municipalities |

|

UN sustainable development goals

- The UN's sustainability goals are the world's joint work plan to eradicate poverty, fight inequality and stop climate change by 2030

- The UN's sustainability goals consist of 17 goals and 169 sub-goals. The goals should act as a common global direction for countries, businesses and civil society

- Many companies, municipalities and organisations choose some sustainability measures to focus more on as part of a larger strategy. In order to make the work with the goals more concrete, it may be wise to divide the sustainability goals into subgoals and link this to selected KPIs

- Beware that the sustainability measures are thematic, and more difficult to use in precise climate reporting

- Read more about reporting on the sustainability goals on the UN SDG Compass